By Ramachandran Rajeev Kumar — 2026-01-10

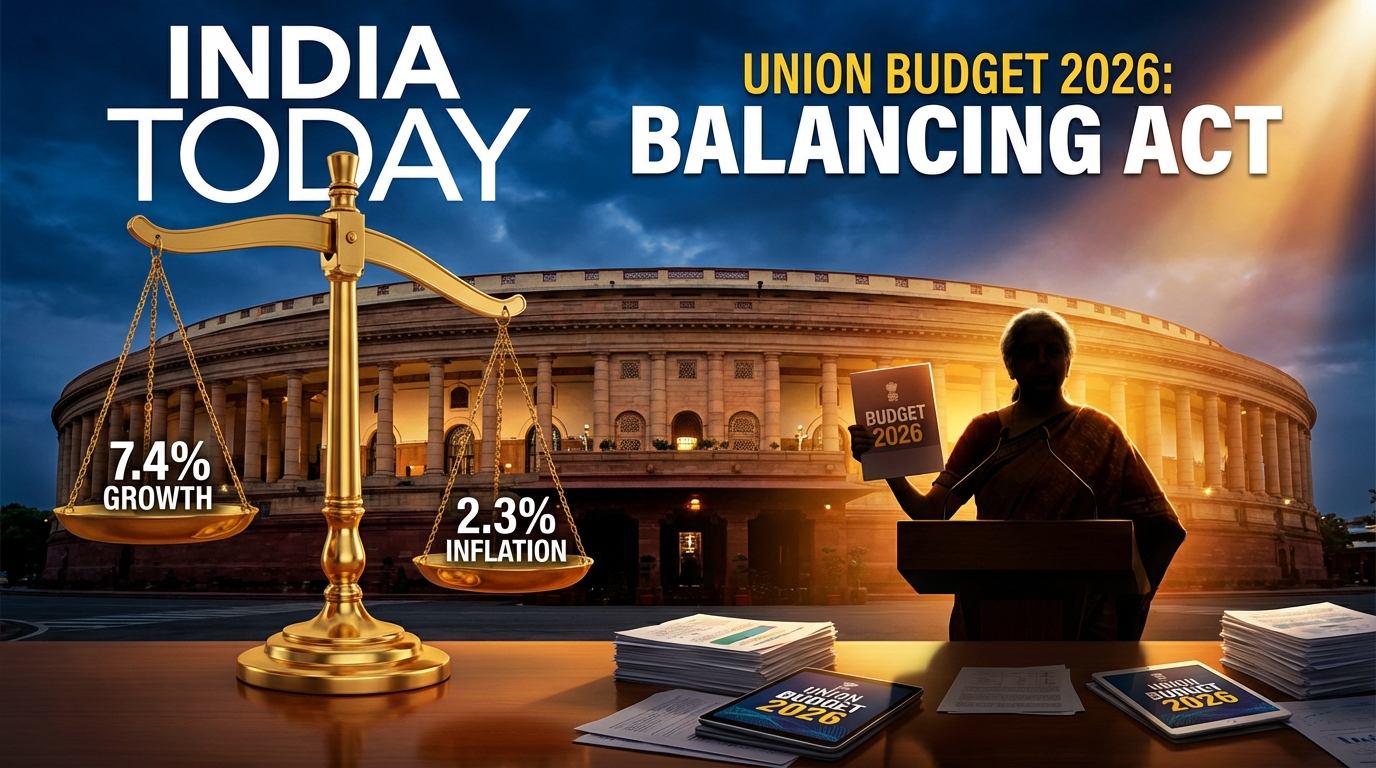

On February 1, 2026 - a Sunday - Finance Minister Nirmala Sitharaman will rise in the Lok Sabha to present her ninth consecutive Union Budget. The session begins January 28 and runs through April 2.

She inherits what the Reserve Bank of India has called a "rare Goldilocks moment": the economy is growing at 7.4%, inflation has averaged just 2.3% (the lowest in years), and fiscal consolidation is on track. The conditions for bold policy-making have rarely been better.

But external headwinds are gathering. US tariffs of 50% on Indian exports threaten key sectors. Tax collections have been slower than hoped. And the fiscal deficit, while narrowing, still constrains spending ambitions.

What can we expect?

The Economic Context

The numbers are genuinely impressive:

| Indicator | FY26 Status |

|---|---|

| GDP Growth | 7.4% (government estimate) |

| Inflation | 2.3% average (until November) |

| Fiscal Deficit | 4.4% of GDP (target) |

| Capital Expenditure | ₹11.2 lakh crore (budgeted) |

| Capex Growth | 32.4% YoY (April-October) |

The RBI forecasts inflation at just 2.0% for FY26 - well below its 4% target. Growth has been resilient despite global turbulence. The first half of FY26 saw 8% real GDP expansion.

The medium-term fiscal trajectory looks sustainable: 4.4% deficit in FY26, declining by 0.4% annually to reach 3.2% by FY29, approaching the FRBM 2018 target of 3%.

This is the macroeconomic inheritance. What does the government plan to do with it?

Five Core Themes

Budget 2026 is expected to center on five priorities:

1. Deregulation & Decriminalization The government wants to reduce compliance burden on businesses. Expect announcements on simplifying regulations, removing outdated laws, and converting criminal penalties for minor offenses into civil penalties. The goal: make India easier to do business in.

2. Exports The 50% US tariffs are biting. MSMEs and manufacturing sectors are feeling the pain. The budget will likely include measures to boost export competitiveness - duty drawbacks, incentives, and support for diversifying export markets.

3. MSMEs Small and medium enterprises are employment engines. Expect credit accessibility initiatives, simplified GST procedures, and support for technology adoption. The government sees MSME revival as essential for both jobs and exports.

4. Implementation Excellence Modi 3.0 has emphasized execution over new schemes. The budget will likely focus on last-mile delivery of existing programs rather than announcing a raft of new initiatives. "Sabka Prayas" (everyone's effort) remains the mantra.

5. Growth Continuity Sustaining 7%+ growth requires continued capital expenditure. The ₹11.2 lakh crore capex target will likely be maintained or modestly increased. Infrastructure spending - roads, railways, urban transport - remains the growth engine.

Tax Changes Expected

Income Tax Relief

The most anticipated change: an increase in the standard deduction under the new tax regime from ₹75,000 to ₹1 lakh. This would put more money in middle-class pockets and encourage migration to the simplified new regime.

The new Income Tax Act 2025, effective April 1, 2026, will replace the 1961 law. Budget 2026 will likely include transitional provisions and clarifications.

Other possibilities:

- Revised safe harbor rules

- Simplified TDS procedures

- Faster dispute resolution mechanisms

- Growth-linked incentives for compliant taxpayers

Technology Incentives

The Production Linked Incentive (PLI) scheme may be extended to new sectors:

- Artificial intelligence

- Space technology

- Robotics

- Advanced computing

Lower import duties on key technology hardware could accompany these incentives.

GST Rationalization

Provisional refunds for inverted duty structures and risk-based sanctioning mechanisms may improve working capital access for businesses.

Sector Allocations

Agriculture

Recent trend: ₹1.18 lakh crore (FY24) → ₹1.41 lakh crore (FY25 RE) → ₹1.38 lakh crore (FY26 BE)

Expect focus on:

- Climate-resilient agriculture

- Cold chain and logistics infrastructure

- Biological inputs scaling

- High-yield seed availability

- Cotton productivity enhancement

- Pulses procurement (four-year program)

Infrastructure

Continued emphasis on capital expenditure:

- PM Gati Shakti integration

- Second asset monetisation plan (2025-30)

- Three-year PPP project pipelines

- National Infrastructure Pipeline expansion

The Confederation of Indian Industry expects higher central capex and increased financial support to states.

Energy & Green Transition

- Electric vehicle incentives

- Green hydrogen initiatives

- Battery storage support

- Clean energy infrastructure

Housing

Affordable housing boost measures remain a priority, though specific allocations await announcement.

Fiscal Challenges

Not everything is rosy.

Tax Collection Pressures: Collections have been slower than projected. Achieving revenue targets requires either better enforcement or downward revision of estimates.

Divestment Shortfall: Asset sale receipts continue to disappoint. The government may need to rely more on borrowing.

State Demands: Opposition-ruled states are demanding greater fiscal transfers. The VB-GRAM-G funding formula (60:40 Centre-State) has intensified tensions.

Global Uncertainty: Trump's tariffs, potential US recession, and geopolitical disruptions create external risks that domestic policy cannot fully mitigate.

What Analysts Say

EY India: Expects the budget to prioritize "growth continuity, tax certainty, and sector-led investment" while balancing fiscal prudence with targeted reforms.

Deloitte: Anticipates measures for "predictable policy roadmap to unlock private capital" and enhance competitiveness.

CII: Wants a new National Infrastructure Pipeline, higher central capex, and increased financial support to states.

The consensus: this budget will be evolutionary, not revolutionary. Consolidation rather than disruption. Implementation rather than announcement.

The FY27 Outlook

Looking ahead:

- Nominal GDP growth target: 10%

- Real GDP growth: 6.5-7.0%

- Inflation: 3.5-4.0%

- Fiscal deficit: 4.0% of GDP

The trajectory remains positive but the margin for error is narrowing. One external shock - a trade war escalation, a Middle East disruption, a financial crisis - could derail the careful planning.

What to Watch For

When Sitharaman rises on February 1, watch for:

- Standard deduction hike - Confirmation of the ₹75k to ₹1 lakh increase

- MSME package - Credit, compliance relief, export support

- Capex target - Maintenance or increase of ₹11.2 lakh crore

- PLI expansion - New sectors receiving incentives

- Agriculture announcements - Climate resilience and productivity focus

- CBAM response - Any measures addressing EU carbon tariffs

- State transfers - How the Centre responds to state fiscal demands

The Goldilocks Risk

The "Goldilocks moment" - not too hot, not too cold - is inherently fragile. The conditions that make bold policy possible are the same conditions that tempt complacency.

India's 7.4% growth is real. So is the 50% tariff wall facing exporters. The 2.3% inflation is welcome. So is the pressure on tax collections.

Budget 2026 will reveal whether the government treats this moment as an opportunity for transformation or merely maintenance of the status quo.

For India's economy, the stakes couldn't be higher.

Budget session begins January 28. Budget presentation February 1. The Goldilocks moment awaits its defining document.