By Ramachandran Rajeev Kumar — 2026-01-08

India's Energy Tightrope: From Caracas to Tehran, A $1 Billion Gamble on Chaos

Two of India's three sanctioned oil suppliers face regime upheaval in the same week. Here's why New Delhi isn't panicking—yet.

In the span of five days, the geopolitical ground beneath India's energy security shifted twice.

On January 3, American special forces captured Venezuelan President Nicolás Maduro in a pre-dawn raid, flying him to a Brooklyn jail where he now awaits trial. Three thousand kilometres east, Iran's Grand Bazaar—the historic heart of Persian commerce—erupted in strikes and street battles as the rial collapsed to 1.47 million against the dollar, with protesters chanting "Death to the Dictator" across 92 cities.

For India, the world's third-largest oil importer, these aren't distant headlines. They're balance sheet items.

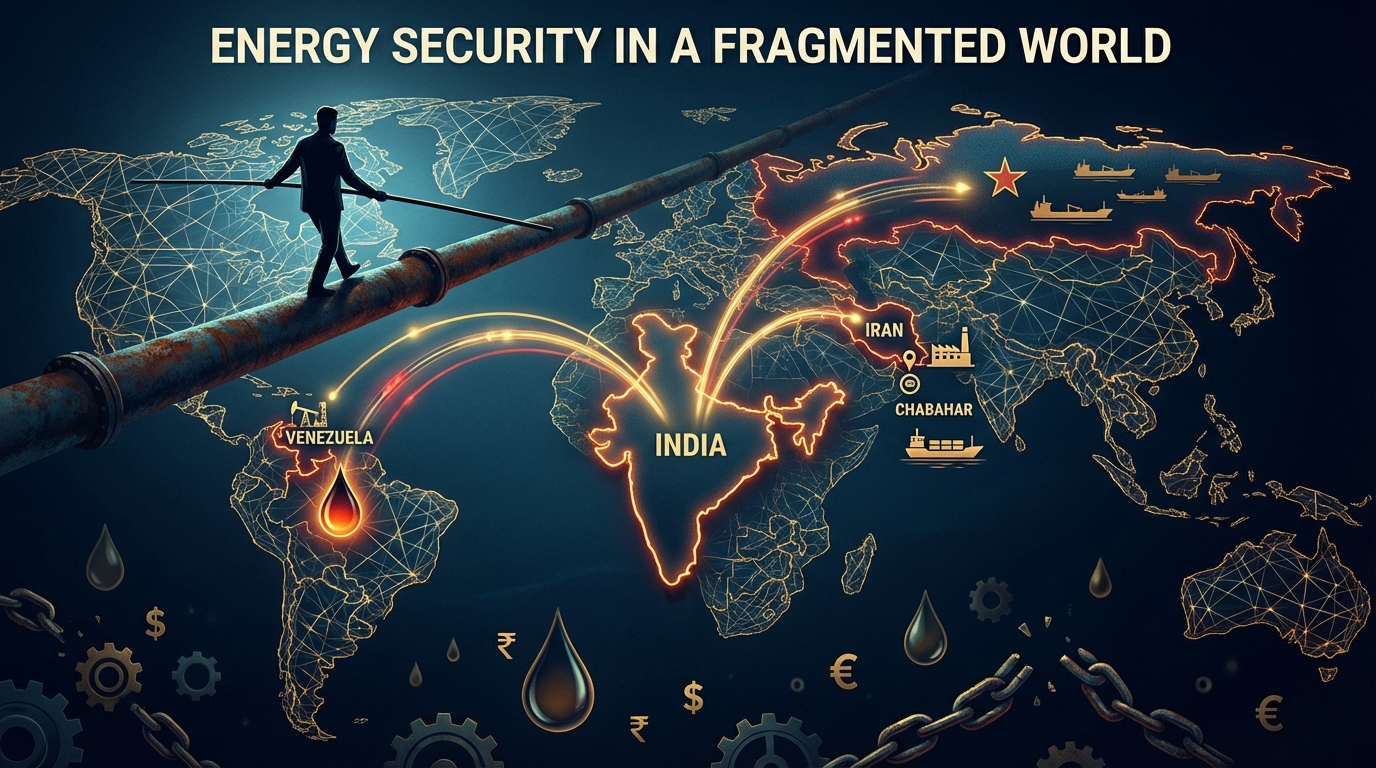

ONGC Videsh has nearly $800 million invested in Venezuelan oil fields and is owed another billion dollars in unpaid dividends. The strategic Chabahar port—India's gateway to Afghanistan and Central Asia—operates on a US sanctions waiver that expires in April. And looming over everything is Russia, which now supplies 36% of India's crude, up from just 1% in 2017.

Three major oil suppliers. All under American sanctions. All in various states of crisis.

Yet in New Delhi's energy corridors, the mood is less panic than cautious calculation. India has spent years building a diversified, pragmatic oil strategy that prioritises commercial flexibility over geopolitical alignment. That strategy is about to face its biggest test.

Venezuela: The Frozen Billions

The relationship between India and Venezuela was once worth $7.2 billion annually. Today, it barely registers.

When the Trump administration first imposed sanctions on Caracas in 2019, Indian refiners—particularly Reliance Industries—were among the last to stop buying Venezuelan crude. The heavy, sulphur-rich oil was perfect for Reliance's Jamnagar refinery, the world's largest, and traded at a $5-8 discount to Brent. It was, in energy economics terms, a bargain.

Then came the sanctions squeeze. India-Venezuela trade collapsed from $5.73 billion in FY2019-20 to just $255 million in the first half of FY2026. Venezuela dropped from a top-ten supplier to 18th place.

But India never fully left.

ONGC Videsh, the overseas arm of India's state oil company, still holds a 40% stake in the San Cristobal oilfield and 11% of the Carabobo-1 heavy oil block. Indian Oil Corporation and Oil India Limited hold smaller positions. Total Indian investment: approximately $770 million.

The problem? These assets have been effectively frozen. San Cristobal, which could produce 80,000-100,000 barrels per day with proper investment, currently limps along at 5,000-10,000 bpd. Worse, Venezuela owes ONGC Videsh roughly $1 billion in accumulated dividends—$536 million confirmed through 2014, with a similar amount for subsequent years that Caracas never audited.

Maduro's capture changes the calculus.

If the United States successfully stabilises Venezuela's oil sector—a significant "if" given the country's decayed infrastructure—India could finally recover its frozen billions. Reliance, notably the only company with an active US Treasury waiver for Venezuelan crude, would be positioned to resume large-scale imports. American oil majors will need partners with refining capacity for Venezuela's difficult crude, and Jamnagar fits the bill.

The optimistic scenario: sanctions lift, oil flows, dividends get paid, and Indian companies participate in rebuilding Venezuela's petroleum industry.

The pessimistic scenario: prolonged chaos, nationalisation disputes, and another decade of frozen assets.

India is betting on pragmatic patience.

Iran: The Ticking Clock

If Venezuela represents frozen opportunity, Iran represents active anxiety.

The numbers from Tehran are staggering. The rial has lost 40% of its value since mid-2025. Inflation runs above 42%. Between 27% and 50% of Iranians now live below the poverty line. On January 6, as bazaar merchants in Mashhad and Tehran shuttered their shops in protest, security forces responded with tear gas and batons. At least 36 people have been killed in ten days of unrest.

Foreign Minister Abbas Araghchi described his own government as being in "survival mode."

This is not 2022, when protests over Mahsa Amini's death challenged the regime but ultimately subsided. The Islamic Republic's regional deterrent—its network of proxies from Hezbollah to Assad's Syria—has been systematically degraded. Assad is gone. Hezbollah is weakened. Iran's nuclear facilities have reportedly suffered significant damage from Israeli and American strikes. The protective architecture that sustained the regime through previous crises has crumbled.

For India, the stakes extend beyond oil.

Chabahar port, developed under a $370 million Indian investment, is the cornerstone of New Delhi's connectivity strategy. It bypasses Pakistan entirely, linking India to Afghanistan, Central Asia, and eventually Russia through the International North-South Transport Corridor. The port has handled over 450 vessels and 8.7 million tonnes of cargo.

In September 2025, Washington revoked the sanctions waiver that had protected Chabahar. After intense Indian lobbying, a six-month extension was granted in October. That extension expires in April 2026.

The questions multiply. If the Islamic Republic falls, what happens to the ten-year port agreement India signed in 2024? Would a successor government honour it? Would American sanctions even apply to a post-theocratic Iran?

Iranian Ambassador Mohammad Fathali insists Chabahar is "a strategic, long-term initiative beyond external pressures." Perhaps. But external pressures have a way of rewriting strategic initiatives.

India's Iran exposure today is modest—just $205 million in crude imports during the first half of 2025, paid through a rupee mechanism designed to avoid US financial networks. The real exposure is strategic: a vision of continental connectivity that runs through an increasingly unstable Tehran.

Russia: The Uncomfortable Anchor

Amid the chaos in Caracas and Tehran, Russia remains India's most reliable sanctioned supplier—which says something about the state of sanctioned suppliers.

The numbers tell a remarkable story. In 2017, Russian crude accounted for 1% of Indian imports. By 2024, that figure had surged to 36%. Between April and November 2025, India imported 60 million tonnes of Russian oil, making Moscow its single largest supplier.

The economics are straightforward. Russian crude, squeezed out of European markets by sanctions, sells at significant discounts. Indian refiners—particularly public sector companies like Indian Oil Corporation and private giants like Reliance—have been happy to absorb the barrels Europe rejected.

Washington is not pleased.

The Trump administration has pressed India to reduce Russian imports, a request New Delhi has handled with characteristic diplomatic ambiguity. According to reports, Indian officials have privately told their American counterparts that any significant reduction in Russian purchases depends on Washington allowing crude imports from Iran and Venezuela.

It is, in essence, a three-way sanctions arbitrage. India is telling the United States: you cannot simultaneously sanction Russia, Iran, and Venezuela while expecting us to maintain energy security. Pick your battles.

This is not defiance. It is pragmatism hardened into policy.

India imports nearly 90% of its crude requirements. The Middle Eastern suppliers—Saudi Arabia, Iraq, UAE, Kuwait—remain the anchor of India's oil basket, valued for proximity, reliability, and refinery compatibility. But Russian discounts have meaningfully reduced India's import bill at a time of global price volatility.

New Delhi's calculation is straightforward: energy security trumps geopolitical tidiness. If that creates friction with Washington, so be it. The lights must stay on.

The Tightrope Walk

India's energy strategists have spent years preparing for exactly this moment—a world where geopolitics, not geology, determines oil flows.

The preparation shows. Despite having three major suppliers under active US sanctions, India has avoided supply disruptions. The diversification strategy—spreading purchases across the Middle East, Russia, Africa, and the Americas—means no single crisis can cripple the system. The rupee payment mechanisms developed for Iran, the Treasury waivers negotiated for Venezuela, the quiet diplomacy maintaining Russian flows—all reflect a bureaucracy that has learned to navigate sanctions regimes.

The positives are real. ONGC could recover $1 billion if Venezuela stabilises. Reliance holds a unique market position for Venezuelan heavy crude. Chabahar has a six-month runway to prove its strategic value. Russian crude continues flowing at discounted prices. India's bargaining leverage with Washington has never been stronger.

But the risks are mounting. Two of three sanctioned suppliers face potential regime change. The Chabahar waiver expires in April with no guarantee of renewal. Trump's interventionist posture—demonstrated in Venezuela—hangs over Tehran. Any oil supply disruption would spike global prices, hurting India disproportionately. The US-India relationship is accumulating friction points.

The fundamental question is whether India's flexibility can survive a world where flexibility itself is under assault. Trump's "maximum pressure" campaigns treat sanctions as binary: comply fully or face consequences. India's entire strategy depends on finding grey zones within that binary.

The Road Ahead

Predicting the future of Venezuela under American stewardship or Iran under a collapsing rial is a fool's errand. What can be said is that India has positioned itself to benefit from multiple outcomes.

If Venezuela stabilises, Indian companies are already there, waiting to restart production and collect dividends. If Iran's regime falls, a successor government unburdened by nuclear sanctions might actually be a better partner for Chabahar. If neither happens—if both countries remain mired in crisis—India's Middle Eastern relationships and Russian flows provide backup.

This is not a strategy of hope. It is a strategy of hedged bets, cultivated options, and deliberate ambiguity.

The next three months will be telling. Chabahar's April deadline looms. Maduro's March court date approaches. Iran's bazaars remain restive. And somewhere in Washington, the next sanctions package is being drafted.

India walks the tightrope. The winds are picking up.

But New Delhi has been here before. And it is still walking.

Ramachandran Rajeev Kumar is the Founder and Editor-in-Chief of BarathVector.