By BarathVector Editorial — 2026-06-12

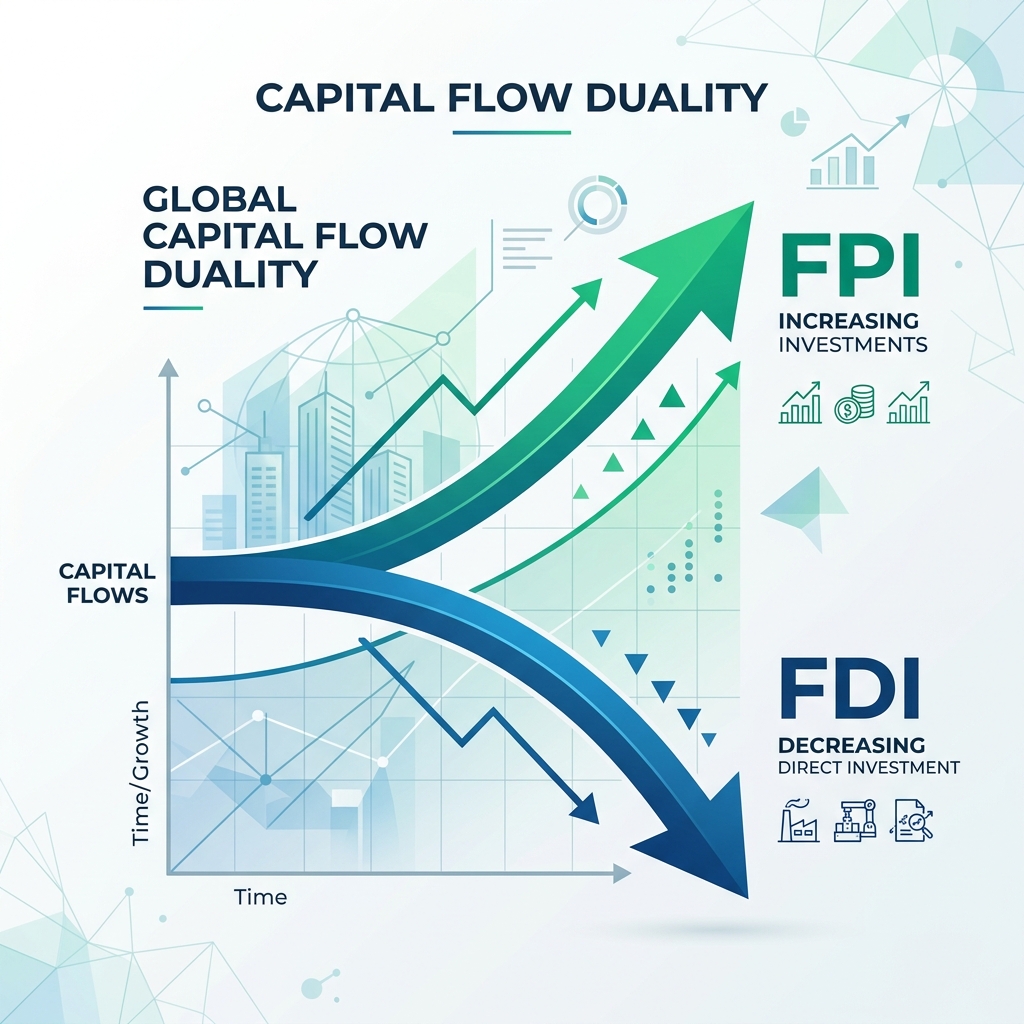

The Divergence in Capital Inflows

India's macroeconomic landscape in 2026 presents a striking paradox. On one hand, domestic growth remains exceptionally strong, with Q1 GDP hitting a resilient 7.8%, cementing India's position as one of the fastest-growing major economies globally. On the other hand, the composition of foreign capital entering the country is undergoing a structural shift that merits careful policy examination.

In recent weeks, the Reserve Bank of India (RBI) announced a series of regulatory relaxations for Foreign Portfolio Investors (FPIs) seeking to invest in government debt and corporate bonds. The objective is clear: attract portfolio capital to keep bond yields stable, support the rupee, and integrate Indian debt markets with global indices.

Simultaneously, however, official balance of payments data has revealed a contraction in net Foreign Direct Investment (FDI). This decline is driven by two factors: an increase in capital repatriation by multinational corporations and a slowdown in new greenfield direct investments.

This duality—rising portfolio capital ("hot money") alongside contracting direct capital ("long-term commitments")—presents a complex puzzle for economic policymakers.

Easing FPI Rules: The Push for Debt Market Integration

The RBI's decision to ease limits and streamline registration processes for FPIs in debt markets is a logical step in India's financial globalization. Following the inclusion of Indian government bonds in major global indices, foreign fund managers have shown a sustained appetite for Indian sovereign debt.

By easing these regulatory barriers, the RBI aims to achieve several goals:

- Diversifying the Investor Base: Spreading sovereign debt holdings across a broader base of international institutional investors reduces the financing pressure on domestic commercial banks.

- Lowering Cost of Borrowing: Increased demand for government securities (G-Secs) helps moderate yields, which in turn reduces the borrowing costs for the government and private corporations.

- Rupee Stability: Constant inflows of portfolio capital provide foreign exchange reserves that allow the RBI to manage currency volatility effectively.

However, the risk of portfolio capital is its inherent volatility. Portfolio investments can be withdrawn rapidly in response to global monetary shifts—such as interest rate changes by the US Federal Reserve or rising geopolitical tensions in West Asia. This makes the economy more sensitive to external shocks.

The FDI Contraction: Analyzing the Repatriation Trend

In contrast to the fluid nature of portfolio flows, Foreign Direct Investment is historically the bedrock of India's capital account. FDI represents long-term institutional trust: the building of factories, the transfer of technology, and the creation of direct employment.

The recent contraction in net FDI is not necessarily a sign that India has lost its investment appeal. Instead, a granular look at the data shows that gross FDI inflows remain stable, but the net figure has shrunk due to:

- Increased Capital Repatriation: Multinational corporations are repatriating profits at higher rates, driven by corporate restructuring and high interest rates in developed markets.

- Strategic Disinvestments: Some foreign venture capital firms are exiting mature Indian startups through initial public offerings (IPOs) or secondary sales, taking advantage of strong domestic equity valuations.

- Global Greenfield Slowdown: High global capital costs have caused multinational corporations to delay large-scale manufacturing expansion projects worldwide.

While exits and profit repatriation are natural signs of a maturing financial market, the contraction in net direct investment means that the physical expansion of manufacturing and technology infrastructure must rely more heavily on domestic capital.

Balancing the Scales: Policy Recommendations

To navigate this capital flow duality without compromising macroeconomic stability, India must pursue a balanced strategy:

1. Guarding Against Portfolio Volatility

While the RBI should continue debt market integration, it must maintain robust macroprudential safeguards. This includes keeping foreign exchange reserves at levels sufficient to cover potential portfolio capital outflows and utilizing sterilized market interventions to prevent FPI surges from distorting domestic liquidity.

2. Streamlining Domestic FDI Realization

To offset the global slowdown in greenfield direct investments, India must accelerate internal ease-of-doing-business reforms. This involves simplifying land acquisition processes, resolving tax disputes through predictable frameworks, and ensuring stable power and transport infrastructure in dedicated industrial corridors.

3. Promoting Long-Term Corporate Reinvestment

Policymakers should consider tax incentives that encourage foreign companies to reinvest their earnings back into their Indian operations rather than repatriating them. Enhancing the attractiveness of local capital reinvestment keeps direct capital within the country, fostering long-term technological and industrial capacity.

Capital flows are a means, not an end. The goal of financial policy must be to channel foreign resources into productive assets that build lasting national capacity. By managing portfolio risks while strengthening the structural foundations for direct investment, India can ensure that its economic expansion remains self-sustaining and resilient to global shifts.