By BarathVector Editorial — 2026-02-19

In 2014, exactly one private company operated in India's space sector. Today, there are more than 325. That number is not a statistic. It is a verdict on a decade of deliberate, if delayed, reform — and it is the most honest measure of how completely India has rewired its relationship with space.

The country's space economy stood at roughly $8.4 billion in 2022, according to a FICCI-EY analysis. By 2033, the target is $44 billion, which would lift India's global share from a marginal 2 percent to 8 percent. That trajectory demands not just engineering ambition but a commercial architecture capable of sustaining it. For the first time in Indian space history, that architecture is being built in earnest.

The Unlock: Policy, Capital, and IN-SPACe

The transformation did not happen overnight, and it did not happen through a single piece of legislation. India's Indian Space Policy 2023 codified what the government had been gesturing toward for years: that ISRO's role was to pioneer, not to monopolise. IN-SPACe — the Indian National Space Promotion and Authorisation Centre — became the institutional engine of that shift. As of January 2026, it has processed more than 658 applications, registered upward of 1,200 startups in its ecosystem, and completed 71 technology transfers from ISRO to private industry.

The FDI reforms of 2024 gave the sector its commercial oxygen. Foreign investors can now hold 100 percent stakes automatically in space component manufacturing, 74 percent in satellite operations, and 49 percent in launch vehicles — a structure calibrated to attract capital while preserving national security boundaries. The Cabinet-approved IN-SPACe venture capital fund of Rs 1,000 crore, roughly $119 million, added a domestic funding backstop for early-stage companies that global investors might overlook.

The cumulative result is $617 million in private funding raised across Indian space startups, with the top ten companies alone holding a confirmed order book of $150 million. This is no longer a scene held together by idealism.

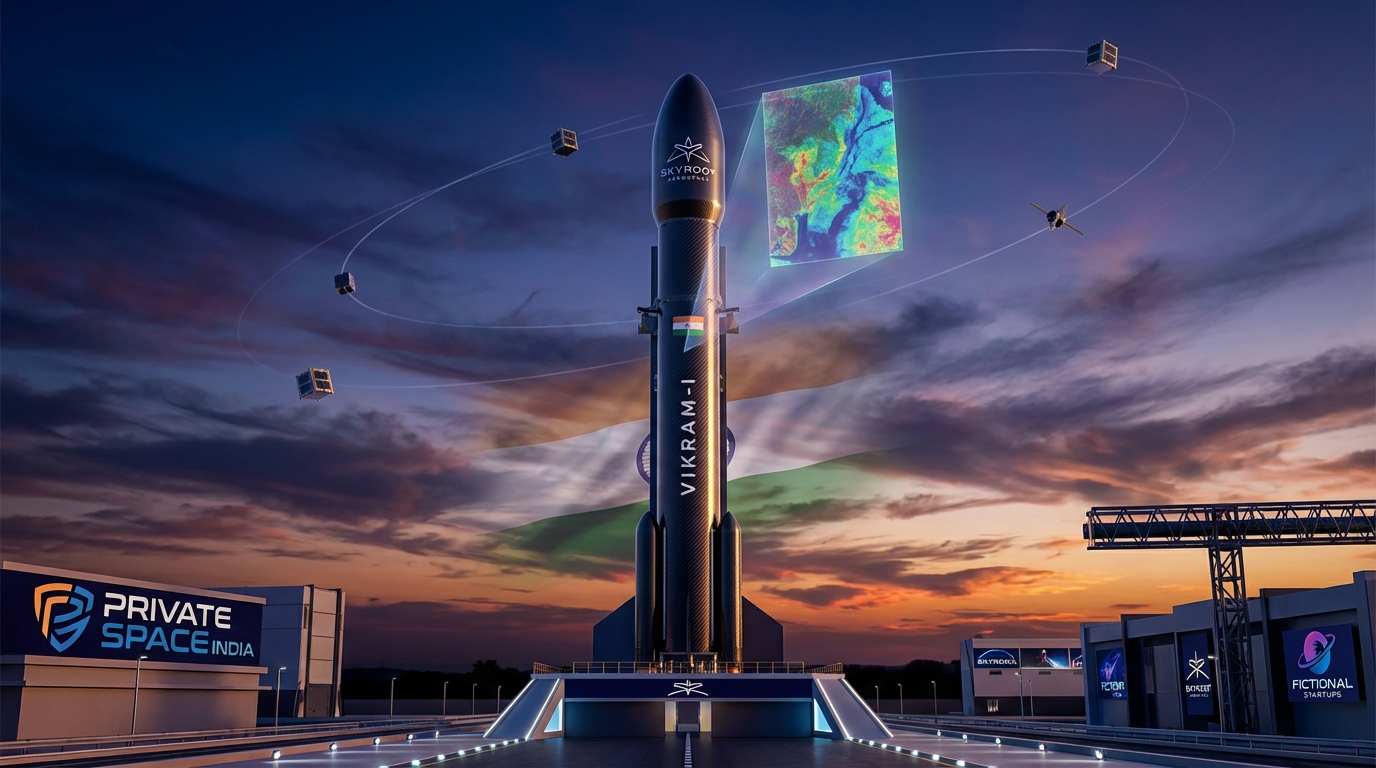

The Companies Doing Real Things Right Now

The most time-sensitive development in Indian commercial space in 2026 is Skyroot Aerospace's Vikram-I. India's first all-carbon-fibre orbital rocket, unveiled by Prime Minister Modi in December 2025, is targeting its first orbital launch in the February-March 2026 window. Skyroot has raised $99.8 million in a Temasek-led pre-Series C round. If Vikram-I reaches orbit, it will not simply be a technological milestone — it will validate the entire premise that Indian private companies can own the launch stack from design to delivery.

Less visible but arguably more consequential in the near term is what Pixxel has achieved. The Bengaluru-based company launched six hyperspectral Firefly satellites aboard a SpaceX Falcon 9 in 2025, each capable of imaging at 135-plus spectral bands with five-metre resolution. Then, in a move that rewrote the Indian Earth Observation market, Pixxel anchored a consortium — alongside Dhruva Space, SatSure, and PierSight — to win IN-SPACe's EO-PPP contract. Twelve satellites. Rs 1,200-plus crore. India's first private national Earth Observation constellation, contracted to deliver imagery that government agencies previously had to source from abroad. This is the kind of contract that turns startups into infrastructure companies.

Agnikul Cosmos has built something most people have not fully registered: India's first private launchpad. Launch Pad 3 at Sriharikota became operational in 2024. The company had already achieved a world first with the Agnilet — the first single-piece 3D-printed rocket engine to fly. The private launchpad matters because launch sovereignty, the ability to decide when and what goes up without queuing behind ISRO's national programme, is the foundational capability for any commercial launch industry. Agnikul now possesses it.

Dhruva Space executed LEAP-01, India's first private commercial rideshare launch, carrying Australian payloads on a SpaceX mission. Bellatrix Aerospace, working on in-space propulsion and orbital transfer vehicles, is already partnering with Skyroot on upper stages and expanding manufacturing to the United States — a signal that Indian space companies are beginning to think globally about their supply chains, not just their customer lists.

The Missing Capstone

The one structural gap that the ecosystem cannot paper over is the Space Activities Bill. The legislation, which would grant IN-SPACe statutory authority, establish a single national licensing regime, create liability caps, and fix the IP rights framework that the 2017 draft had stripped away from space inventors entirely, remains in inter-ministerial consultation. It has not been tabled in parliament.

This matters for reasons that go beyond regulatory tidiness. IN-SPACe currently runs on executive orders, which means its authority can be redrawn with a change of government or a shift in bureaucratic consensus. When a private operator wins a contract worth hundreds of crores and needs insurance, debt financing, or foreign partnership agreements, counterparties want statutory certainty, not administrative discretion.

The Devas-Antrix arbitration case — a 2015 dispute that ultimately cost India $562 million — remains the cautionary precedent. A clear liability and licensing framework would not eliminate commercial disputes, but it would establish the rules under which they are resolved. Every month the bill remains in consultation is a month that serious institutional investors are pricing in regulatory risk.

An additional structural concern: IN-SPACe currently handles its own appeals, a conflict of interest that the bill is expected to address. Multi-ministry clearances are still required even after IN-SPACe grants approval, adding friction that accumulated approvals alone cannot eliminate.

The Gap to Watch

The enthusiasm of India's political leadership for space has not always translated into funding consistency. The space department's budget for 2025-26 stands at Rs 13,415 crore, a significant increase from Rs 5,615 crore in 2013-14. But the Economic Survey for 2025-26 notes that effective capital expenditure has declined in real terms, and the department has a documented pattern of failing to fully utilise annual allocations. The 2026-27 budget carried only a 2 percent marginal increase. When the government's own targets require 50 rocket launches per year and five space unicorns within five years — both commitments made publicly by Prime Minister Modi — the budget arithmetic deserves scrutiny.

The Trajectory

By 2033, the FICCI-EY projections see the Indian launch market reaching $3.5 billion, SATCOM at $14.8 billion, Earth Observation at $8 billion, and space exports at $11 billion. Against a global space economy projected to exceed $1.8 trillion by 2035, a $44 billion Indian sector would represent a genuine industrial transformation — not a larger version of the prestige programme that put Mangalyaan in Mars orbit for less than the cost of a Hollywood film.

India has already demonstrated it can reach space cheaply and creatively. The decade between 2014 and 2025 proved it can build an ecosystem around that capability. The decade between 2025 and 2035 will determine whether that ecosystem produces global competitors or remains a promising domestic story.

Vikram-I on the launchpad is the most honest symbol of where India stands. The rocket is ready. The question is whether the legislative architecture will catch up before the launch window closes.